Many of my creative friends have side projects while Jake’s friends have Twitch streams bringing in extra income, and I consistently find that many independent contractors don’t understand estimated tax payments. We all owe the IRS an annual tax return in which we declare all of our income for the year–even if we didn’t receive a 1099 from PayPal or another payor. (We Californians owe the state Franchise Tax Board as well.) Most new businesspeople take the phrase estimated taxes literally. Sounds smart, like budgeting, but isn’t actually required by law. However, for the self-employed, estimated taxes are required by tax law to be submitted every quarter during the taxable year (meaning when you file your annual return for last year, you should have already made four pre-payments towards your federal taxes for the prior year).

When you are paid as an employee your employer withholds taxes on your paycheck, as well as covers the employer share of some of those taxes, and you receive a W-2 at the end of the year showing all the payments that have been made regularly over the course of your employment. This means as you earned income, the taxes were remitted on a timely basis. When you are paid as an independent contractor—meaning you typically have a contract specifying a payment schedule or submit invoices—your customers do not withhold any taxes for you, and it’s up to you to make timely tax payments as you earn the money. You cannot wait until the following April and send one big check with your tax return or you will incur penalties for the underpayment of estimated taxes. (You can calculate these with your return using Form 2210, but if you don’t, the IRS will, and will send you a bill. It may take some time for them to do this, but they will catch this common error and come calling for the penalties and the increased amount of interest now due to them.)

If you owe less than $1,000, there will not be any penalty. For most people, as long as you pay 90% of what you actually end up owing for the current year (in the actual quarters in which you earned the income), you are safe. Alternatively, you can pay 100% of what you paid last year, unless your income is greater than $150,000, then the IRS requires 110% of what you paid the prior year to ensure you are penalty-proof.

For 2018, but when you get your final 2017 return done, look at your total taxes owed. Subtract from that total the amount any employer can be expected to remit for you over the course of the year. Take your current pay stub and multiply the income taxes withheld and remitted on that single paycheck by the number of paychecks you receive in a year. Assuming you pretty much make your money equally over the course of the year, you can divide the balance by four and download a 1040-ES coupon (page 11) to remit these sums each quarter on the due dates listed to stay clear of penalties and interest. Note that while the payments are typically due the 15th after the calendar quarter ends, they second payment is due a month earlier—on June 15, before the quarter ends. (This is true for the California as well, the 540-ES stubs are here.)

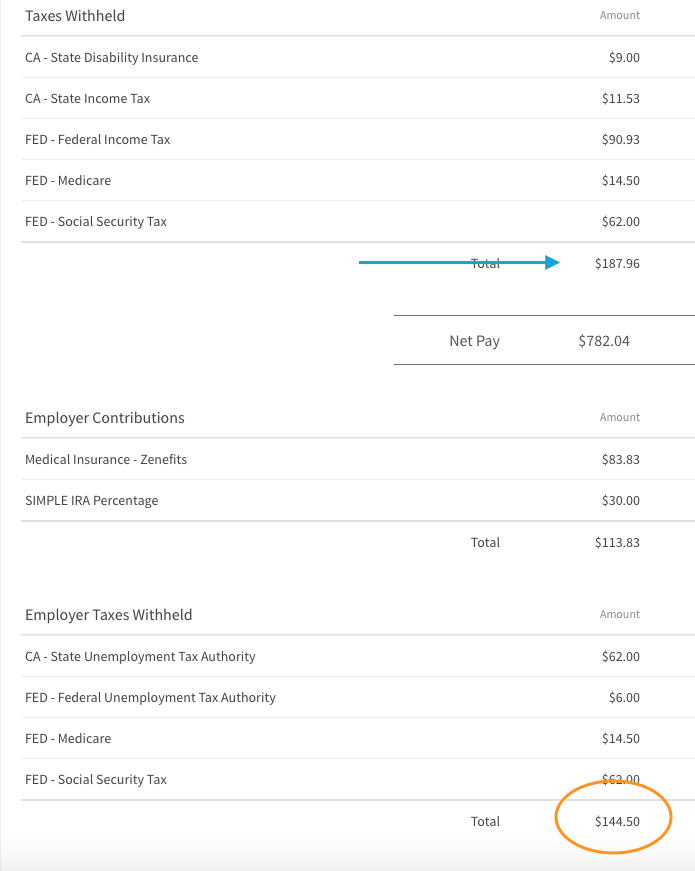

As I used a fictional Overwatch League player, making the minimum guaranteed annual salary of $50,000 before, I’ll stick with that example here. Now we’ll assume that this player has Twitch revenues of $1,000/month coming in as an independent contractor, which probably means he also has some tips coming in via PayPal, which should also be declared, so let’s say tips average $500/month ($1,500 x 12 = $18,000/year). The OWL team will be remitting taxes based on the information provided by the player, and as most of the players are single, childless, and probably not home-owners yet (so they have few of the deductions the tax code favors), if they accurately completed their W-4 the taxes being submitted are pretty high, which, given the $1,000 tax due grace amount, gives the casual side hustle a safer margin. On this salary, the federal income taxes should be about $500/month, of $6,000/year. If on his 2017 return the player owed $9,000 in income taxes, the penalty-proof amount to remit would be the extra $3,000, or $750/quarter on the 1040-ES. Keep in mind that 1040-ES is your estimate of what you owe so there’s no guarantee it ends up being the right amount for the year. This just guarantees you don’t have to give the federal or state tax departments more money than required. The smart rule of budgeting would be to take a set amount of your 1099 income each month and put it in a separate savings account for taxes, so whatever you owe, you can pay promptly with submission of your tax return.

Payroll taxes are calculated based on the income rates for that salary, so while the OWL team is correctly remitting for a person who makes $50,000 a year, the player actually makes $68,000 a year. Not only is $18,000 going untaxed all year, but the player could have bumped into higher tax brackets on some of the salaried $50,000, meaning not enough of it was being remitted as income tax. With the new 2018 laws, this wouldn’t be true for these dollar amounts, but it’s worth being conceptually aware that marginal tax brackets exist and you can shift into a higher one for some of your salaried dollars.

There is an alternative option for anyone with a paycheck. You can ask your employer to let you adjust your W-4, and have additional amounts remitted each paycheck for your state and federal taxes. In this case, if the player is paid monthly, he could complete his W-4 so that an extra $250/month was being remitted towards federal income tax, thus meeting the $750/quarter amount he expects to be correct for 2018. This makes the paycheck a little heavily taxed, so that he doesn’t have to worry about the Twitch and PayPal income being untaxed in real time. Any way you get there, you want to be sure you are remitting taxes as you owe them, as you earn the income, so you don’t pay more than what you should owe in interest and penalties.